Sunday, 8.40pm

Sheffield, U.K.

Debt is like any other trap, easy enough to get into, but hard enough to get out of. – Josh Billings

I’ve been browsing through Donella H. Meadow’s Thinking in systems and realising that I was completely wrong about things I took for granted.

For example, she talks about what happens when there are two competing things happening at the same time.

The simplest example is the problem you have in winter managing your room temperature.

If you left your house for a week or so with the heating off what would happen?

The heat in the house would flow outside through the windows and gaps until the outside temperature and inside temperature were pretty much the same.

Now, when you get back and don’t want to spend your time shivering, you turn up the thermostat.

This monitors the gap between what you want and what the room temperature is and turns on your radiators until the gap between the setting and the temperature is nothing.

So far so simple.

Now, some of you may have experienced an argument with the others that live in your house that goes something like this.

You want to save money and so keep the thermostat at 20 degrees because that should be enough.

The other people in the house, little and large, disagree and push it up to 25.

I always thought it was reasonable to assume that if the setting was 20 then the room temperature would end up at 20 and then the thing would turn off.

That’s an example of doing the wrong thing because it seems logical – and the problem comes from forgetting about the other loop – the one constantly causing heat to leak out of your house.

You need to figure out how to deal with the losses that are happening at the same time as the gains.

Meadows says that people normally learn to set the thermostat at a higher temperature to get the level of comfort they want – which is why it turns out that I’m wrong and the others are right to do what they’re doing.

Meadows points out that this issue is not really that serious – you can muddle your way through to a solution but it can cause all kinds of problems in other situations – and your bank knows this.

The key point is this – the action you take can only affect the future – and you take action after realising that there is a gap – which happens after some time.

In other words there is a delay between changing the setting and the change in the room temperature (the stock).

The delays in the system are important – and the delays happen from both sides, the thing that causes the stock to increase and the thing that causes it to decrease.

And this is where we come to debt…

Meadows writes, “If you want to pay off your credit card (or the national debt), you have to raise your repayment rate high enough to cover the charges you incur while you’re paying (including interest).”

So that’s something else I’ve been doing wrong.

If you pay for holidays and online purchases on a credit card you might have experienced the shock that comes with paying off a large balance every month.

Even if you’re good and pay it all off it never seems to disappear – it’s like this anchor that’s attached to you every month.

Well, that’s because your credit card purchases take place in a similar way to the thermostat model.

So, I thought I’d try this out – get a year’s worth of credit card expenses and see how the system keeps us in debt.

Well, it turns out that the banks don’t want you to do the modelling.

If I were suspicious, and I am, I’d think that the fact that they provide only three months of transactions to download as a csv suggests they don’t want you to look too closely.

And then, the nature of the csv, which makes sure all numeric fields come in as text and have additional symbols that make it hard to add everything up, suggests that someone is trying to raise the barriers to analysis.

Or am I too cynical?

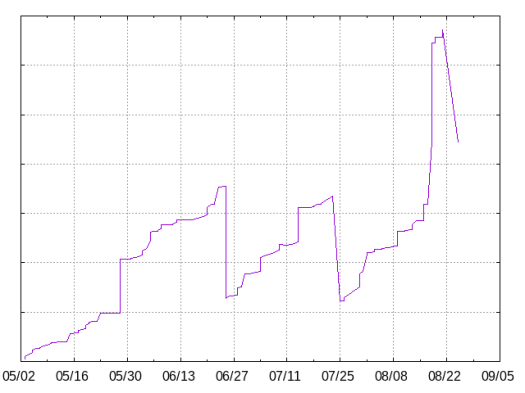

Anyway, the spending pattern that happens is shown in the chart below.

What you’ll see is that although everything is paid off every month (the sharp downward line) the leakage in additional costs over the course of the month means that there is a constant level of debt.

What happens if you pay a little bit extra off every month?

What happens is in this next chart.

What you see is that your total debt can go to zero – but only if you pay more than you need to.

This is actually a very important point because we spend so much of our time trying to hit targets but if our mental model doesn’t take into account all the factors that matter we won’t reach our goals.

For example, I aim to write every day but I haven’t written for 13 days for a variety of reasons.

Last year out of 365 writing days I managed 251 posts – that’s more than a hundred days that just leaked away.

If you’re trying to lose weight by cutting calories, perhaps instead of targeting 2,000 a day you need to go for 1,800 because there’s going to be leakage.

If you need to raise cash go for $1.2 million rather than $800k.

Now, you might argue, this is just common sense.

Surely this is just setting “stretch goals”?

I’d argue that once you understand the model it’s more than that – it’s realising that you need to look at the whole picture.

Meadows writes, “The human mind seems to focus more easily on stocks than on flows. On top of that, when we do focus on flows, we tend to focus on inflows more easily than on outflows. Therefore, we sometimes miss seeing that we can fill a bathtub not only by increasing the inflow rate, but also by decreasing the outflow rate.”

The thermostat problem seems small – but it’s the essentially the same problem as the issue of climate change.

And no one would argue that’s an easy one to set right.

Cheers,

Karthik Suresh

p.s two interesting links