Steven Landsburg introduced his book “The armchair economist” with the words Most of economics can be summarized in four words: “People respond to incentives.” The rest is commentary.

That is the start of economic analysis. Supply and demand curves. p is for supply, q is for demand and they have a linear relationship.

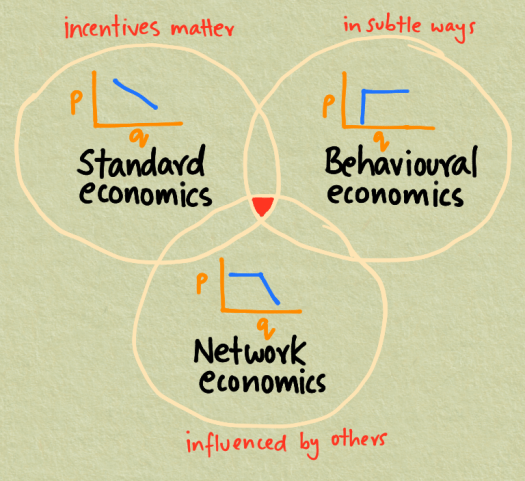

In standard economics, demand (q) rises as price (p) decreases – and that is one of the first charts we learn in an economics class.

This assumes that people are rational, evaluating the costs and benefits of options in a logical way and taking actions that maximise their profit or utility – the satisfaction we get from a purchase.

But people aren’t rational. In reality, we are driven by emotion and our animal brains and this is where behavioural economics comes in.

For example, under pressure, we go into flight or fight mode and make decisions based on gut instinct – and that is what has kept our species alive.

Another way in which people aren’t rational is how they react to an unfair deal.

Take, for example, a game where people get a sum of money. One person gets to decide the share of the prize – and the other can accept or reject the offer.

In theory, any amount more than zero should be accepted by the rational recipient. In practice, many don’t accept anything less than a share closer to a fair one – a 50/50 split.

Shown as a chart, this might mean that demand is fixed at a range of prices, but over a particular level it increases.

The factors affecting the shift in mentality are more subtle – they are affected by the emotional processing that goes on inside our heads.

Then we have network economics. In this view, what we do depends on what others do – we watch and copy behaviour.

This is most visible in online behaviour. The top three results on Google get virtually all the traffic. There can be huge differences in views for very similar videos.

So, in network economics, price has little effect until we reach a tipping point, after which demand increases rapidly – but the tipping point is determined by the network effect.

The charts in the picture may not describe the situation accurately – real life is more complex than we can show in this way – but the interesting point is the impact it has for the choices we make as producers and consumers.

As producers, we can’t simply make better mousetraps cheaper and expect people to buy them.

Instead, we need to create cheaper products, think about how people will react emotionally to what we are selling and leverage the economics of networks to get our products to scale.

As consumers, we need to be mindful that price is no longer representative of value in many cases – so we need to be wary of using that as a heuristic or rule of thumb.

We also need to realize that producers use increasingly sophisticated techniques to appeal to our emotions, from subtle emotional cues to overt use of celebrity endorsements.

Finally, by copying what everyone else is doing, we may be missing out much that has real value and settling for the fads of the moment.

But, the changing world also offers unparalleled opportunities for those who are positioned where the three economic approaches overlap.

In the middle there, with a little bit of luck, new superstars emerge.