Monday, 5.26am

Sheffield, U.K.

All great artists draw from the same resource: the human heart, which tells us that we are all more alike than we are unalike. – Maya Angelou

So far in this Getting Started book project I’ve written about how to appreciate yourself, what you have achieved so far, and your situation, where you are right now.

We’ve also spent a little time looking at networks, and how to break into them and use the ones you already have.

Now its time to look at resources – a few different ones – because what you can do is quite often determined by what you have.

But how do you work out what you have, how to use it and how that will help?

Let’s look at that in more detail for the next few posts.

Making accounting interesting

Accounting can get complicated when you look into it – but that’s partly because companies “manage” the numbers rather than report on them and much of what goes into a report is interpretation, what you think you can get away with under the rules.

It’s a way of manipulating the reporting of reality.

That’s not really what we’re interested in.

We want to see if the methods of accounting can help us make sense of reality.

And one of the best ways I’ve seen this being applied is in Robert Kiyosaki’s book “Rich Dad Poor Dad”.

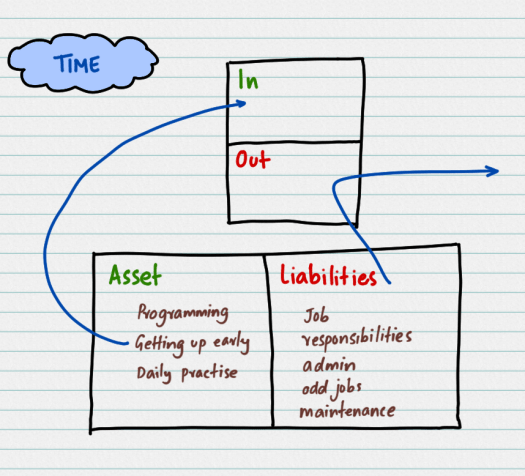

The picture above shows the traditional American style accounting report – with a profit and loss (P&L) statement and a balance sheet.

There are four words that you need to understand when it comes to these reports.

They are income, expense, assets and liabilities.

Income is something you get, something comes in, expenses are something you pay, and something goes out.

Now, you probably understand what assets and assets and liabilities mean but Kiyosaki has a nice definition that links everything together.

He writes, “Assets put money in your pocket, whether you work or not, and liabilities take money from your pocket”.

This is not an accounting definition – but it is a very useful idea – and something that you could generalise and use in other situations.

Let’s see how that might work.

What are resources?

If you were to put down a list of resources you have it might include things like money, time, knowledge, skills, networks, partners and so on.

You might include personal qualities: determination, courage, grit, persistence.

All these things are clearly not equivalent.

Money is something you can put in a bank, accumulate, get more of and spend of.

Time, on the other hand, is fixed. You can’t make more of it but have to use what you have.

Knowledge is something you have, or don’t have.

Once you get it, it can’t be taken away from you, even if you give it all away you haven’t lost the knowledge you have.

This explanation is starting to get a little complicated because it’s a mix of accounting, but it’s also systems dynamics, and both approaches are not quite rich enough or flexible enough to really get the idea.

I may have to rework this post entirely to see if I can create a better model to capture what I’m trying to get across here.

But let’s carry on for now and see where we end up.

What’s important is working out what you have and what that means for you.

And let’s work out what that means when it comes to time, for example.

What happens to your time?

You have a fixed amount of time, the same 24 hours as everyone else.

All you can do is allocate your time to different activities, remembering that sleeping and eating and life in general take up quite a lot.

If you look at this through the accounting lens in the picture above, some of the things you do help give you time and other things take time away.

If you think of these things as assets and liabilities, assets release your time and liabilities consume your time.

Or alternatively, assets multiply your time.

How would you fill in your list of assets and liabilities in these tables?

As I thought about the things that I’d put on my list I started with programming.

For most of my career the ability to program has released time and multiplied time for me.

When I was a research student I automated my entire work pipeline, coming into the office in the morning, setting up the flow and letting the computers work away, doing their thing, while I had coffee and chatted with my friends.

Even now, everything I do is made easier because it’s done using programming knowledge that helps speed up the process and does in seconds or minutes what takes many people hours or days.

Another thing that releases time is getting up early or working late – when everyone else is asleep or busy.

If you look at the timestamps on these posts you’ll see that’s the case.

Then there’s daily practise – committing to doing something every day – like writing these posts in the first place.

That kind of daily work helps build up the skills to do the task better and more efficiently over time.

These assets help you do more of what you want to do.

Liabilities, on the other hand, are the things that make you spend time on the things you don’t want to do, or rather would not do.

The biggest thing on the list here is probably your job.

Most people, if they could, would rather do their own thing than clock in for work every day.

Perhaps you have a range of responsibilities – it might include tasks like caring for someone else.

Something you have to do and would feel bad about not doing – but still something that consumes your time.

And then there are all the small time-wasters, the administration, the jobs around the house, maintenance and gardening.

Of course, if spending time with your family is something you like doing and doing the gardening and washing your car gives you a sense of peace and satisfaction, then maybe those things are assets, ways to help you de-stress.

Just like in real accounting, it’s all about interpretation, whether something you do increases your satisfaction with how that time is spent.

It’s not quite that simple, however

If you look at things and how they impact your time then you’ll put them in certain places on your balance sheet.

But, if you look at them in they way they impact other things then you might take a different view.

When it comes to money, for example, is your job an asset?

After all, it gives you money.

And all these things that you do as a hobby – programming, writing every day – don’t make money immediately.

So does that mean they’re actually liabilities?

Or is it actually about what they are at any point in time, just like a balance sheet is actually a snapshot that’s only right for that instant.

A job is an asset while you’re trying to build your business but it becomes a liability once you’re making a decent income from your side hustle?

And things like daily practise are great as a hobby but do they actually get in the way if your objective is to be noticed and catapulted into a senior role in your organisation, perhaps even be the youngest person to lead it?

What you put where depends on what you’re trying to do.

Or the interplay between what you do, what that impacts and what emerges as a result.

It’s complicated and complex – but life is not about easy choices and boxes with straight lines.

It’s messy and mixed up, and you have to work out what it means for you.

The simple answer is usually not the right answer for you in your situation.

Let’s try and address this again in the next post and see if we can build a better model.

Cheers,

Karthik Suresh

2 Replies to “How To Assess And Analyse The Resources At Your Disposal”